MetaMask's mUSD: An ambitious work to leverage the stablecoin market with hundreds of millions of users

Written by: Prathik Desai

Compiled by: Block unicorn

Weekly has felt déjà vu lately – another stablecoin launch, another attempt to change the direction of value. First, we saw a bidding war for Hyperliquid to issue USDH; We then discussed the verticalization trend for capturing US Treasury yields. Now, it's MetaMask's native mUSD. What are all these strategies connected to? Distribution capacity.

Distribution capability has become a cheat code, not only in the crypto space but also in various sectors as a way to build a thriving business model. If your community has millions of users, why not take advantage of it and put tokens directly into their hands? However, this doesn't always work. Telegram has tried to achieve this with TON, claiming to have 500 million message users, but these users have never migrated on-chain. Facebook has also tried to do this with Libra, firmly believing that its billions of social media accounts can form the basis of a new currency. In theory, these two projects seemed destined to succeed, but in practice they failed.

This is probably why MetaMask's mUSD (with fox ears and a "$" symbol at the top) caught my attention. At first glance, it looks like no other stablecoin – backed by regulated short-term U.S. Treasuries and issued through a framework developed by Bridge.xyz using the M0 protocol.

But how doesMetamask's mUSD differ in the current $300 billion stablecoin market dominated by a duopoly?

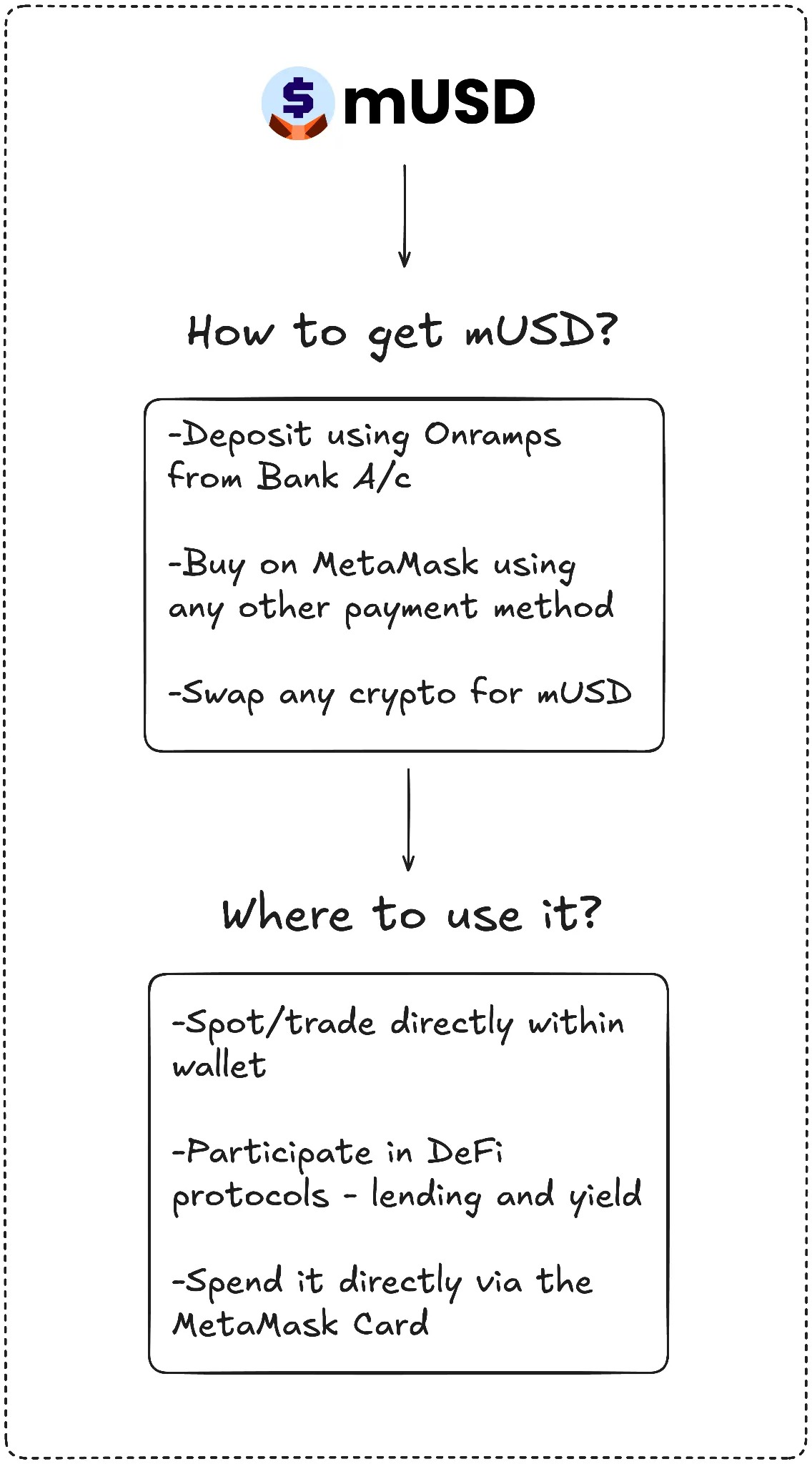

MetaMask may be entering a competitive space, but it has a unique selling point that no other competitor can match: distribution. With 100 million annual active users worldwide, MetaMask's user base is almost unmatched. mUSD will also be the first stablecoin to be natively issued in self-custody wallets, allowing users to buy, swap, and even spend in-store with a MetaMask card with fiat currencies. Users no longer need to find between exchanges, bridge across chains, or deal with adding custom tokens.

Telegram does not have this fit between the product and user behavior, while MetaMask does. Telegram is trying to move its message users to the blockchain for decentralized finance applications. MetaMask, on the other hand, enhances the user experience by integrating native stablecoins into the app.

The data shows that the adoption of this initiative is very fast.

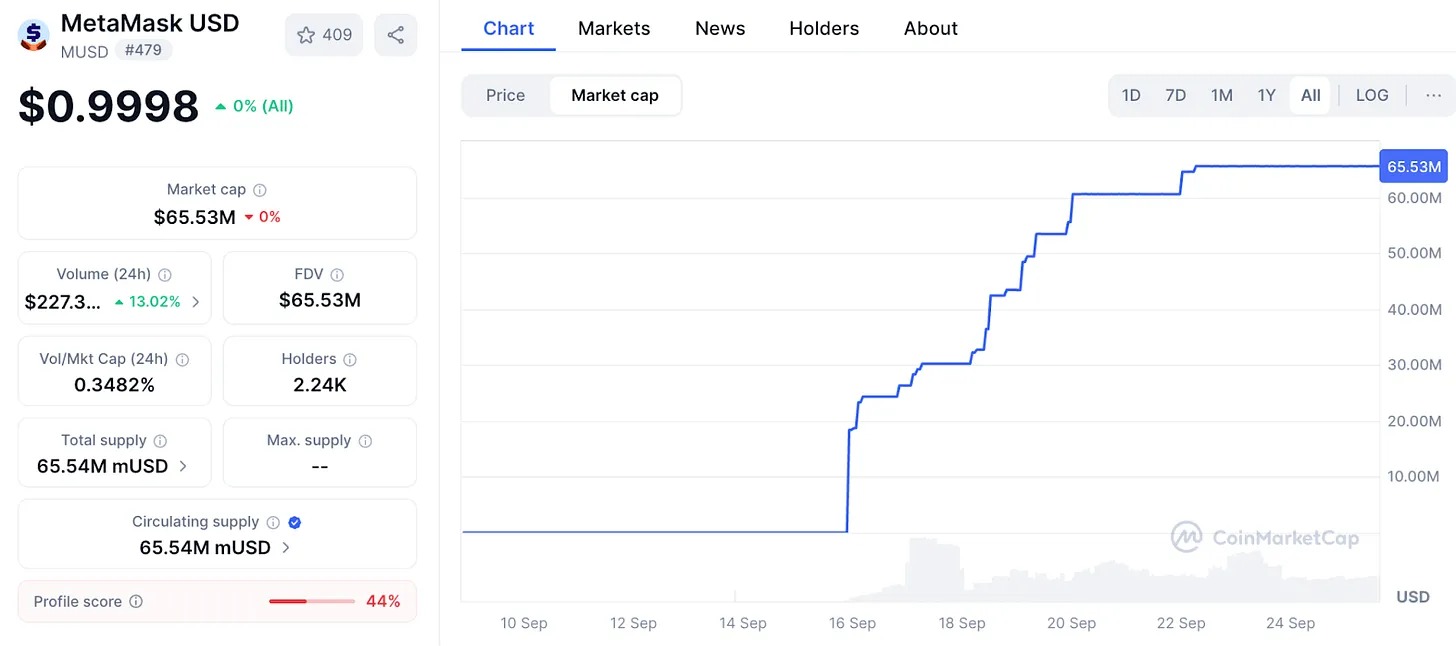

MetaMask's mUSD market cap has surged from $25 million to $65 million in less than a week. Nearly 90% of this funding comes from ConsenSys' internal Layer 2 platform, Linea, indicating that MetaMask's interface is effective in channeling liquidity. This leverage is similar to past operations by exchanges: in 2022, Binance automatically converted deposits into BUSD, causing circulation to soar overnight. Whoever controls the user controls the token. With over 30 million monthly active users, MetaMask has the largest number of users in the Web3 space.

– >

– >

this distribution capability will set MetaMask apart from early players who have failed to build a sustainable stablecoin.

Telegram's grand plans have partly failed due to regulatory issues. MetaMask circumvents this issue by partnering with Bridge, a Stripe-owned issuer, and backing each token with short-term Treasury bonds. This meets regulatory requirements, and the new GENIUS Act in the United States provides a legal framework from day one. Liquidity will also be key. MetaMask is injecting Linea's DeFi with mUSD trading pairs, betting that its internal network will solidify its applications.

However, distribution does not guarantee success. The biggest challenge for MetaMask will come from the existing giants, especially in a market already dominated by several giants.

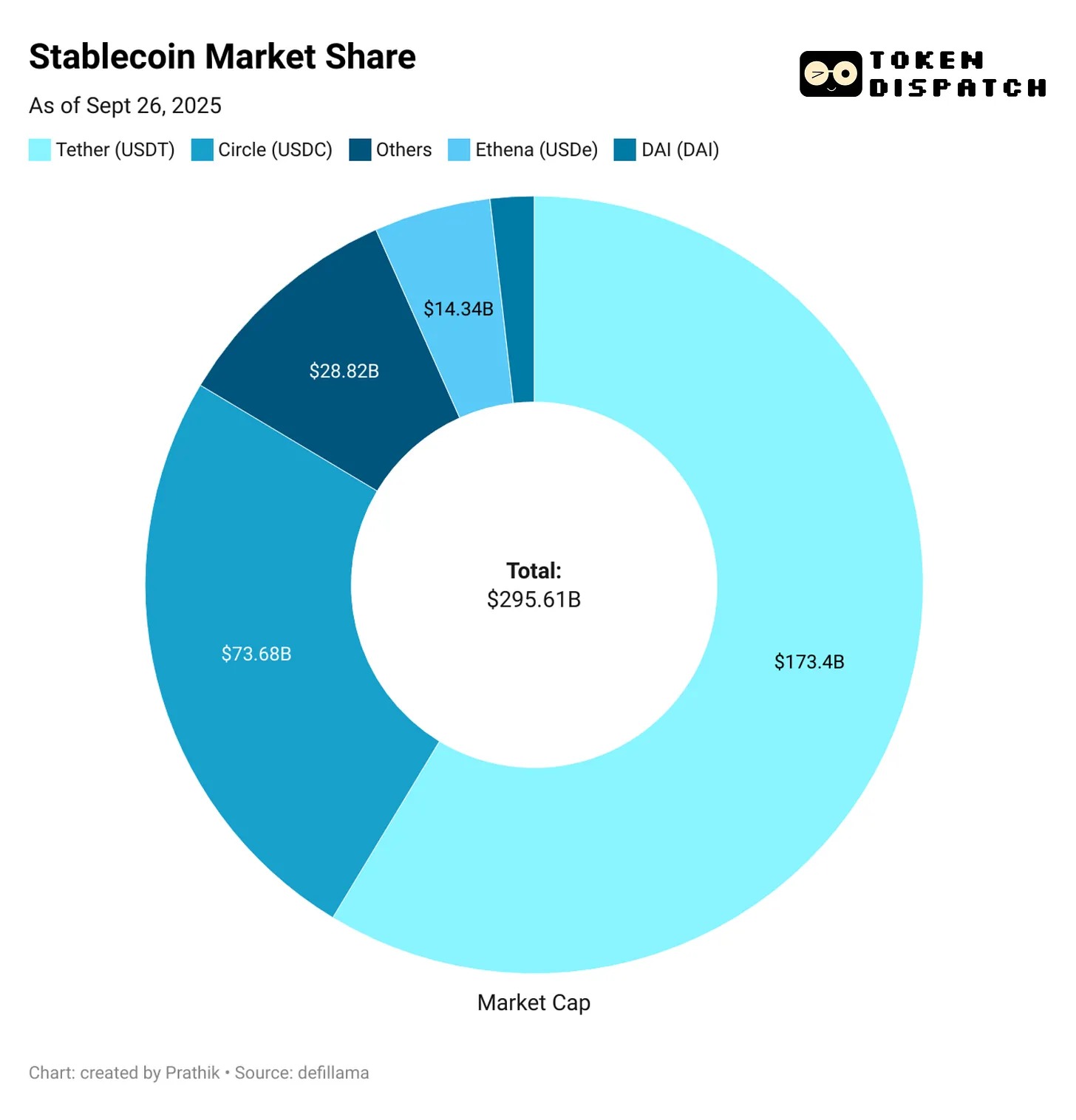

Tether's USDT and Circle's USDC have captured nearly 85% of the market share of all stablecoins. In third place is Ethena's USDe, with a whopping $14 billion in circulation, attracting users due to its earnings. Hyperliquid's USDH has just gone live and aims to put exchange deposits back into its ecosystem.

This brings me back to the question: what exactly does MetaMask want mUSD to be?

USDT and USDC seem unlikely to emerge as direct challengers. Liquidity, exchange listings, and user habits are all beneficial for the incumbent giant. mUSD may not need to compete head-to-head. Just as I expected Hyperliquid's USDH to benefit its ecosystem by delivering more value to the community, mUSD is likely also to capture more value from existing users.

mUSD will be preferred whenever a new user deposits through Transak, whenever someone exchanges ETH for a new stablecoin inside MetaMask, and whenever they swipe their MetaMask card in the store. This integrates stablecoins as the default option within the network.

It reminds me of those days when I needed to bridge USDC between Ethereum, Solana, Arbitrum, and Polygon, depending on what I needed to do with my stablecoin.

And mUSD puts an end to all the tedious bridging and swapping.

– >

– >

Then there's another important takeaway: yield.

With mUSD, MetaMask can generate yield from the U.S. Treasury bonds backing the token. Every $1 billion in circulation means tens of millions of dollars in interest flows back to ConsenSys each year. This will transform the wallet from a cost center to a profit engine.

If just $1 billion of mUSD were backed by the equivalent of U.S. Treasuries, it could earn $40 million in interest income annually from the proceeds. In contrast, MetaMask generated $67 million in revenue from the fees it collected last year.

This could open up another passive, significant revenue stream for MetaMask.

However, there is one factor that upsets me. For years, I have considered wallets to be neutral signing and sending tools. mUSD blurs this line, turning the neutral infrastructure tool I once trusted into a business unit that profits from my deposits.

Therefore, distribution is both an advantage and a risk. It could make mUSD the default sticky choice or raise questions about bias and locking. If MetaMask adjusts the exchange process to make the path of its own tokens cheaper or prioritized display, this could make the world of open finance less open.

There is also the problem of fragmentation.

If each decentralized wallet started issuing its own dollar, it could create multiple closed currencies instead of the interchangeable USDT/USDC duopoly we have now.

I don't know where this is going. MetaMask does a good job of closing the financial cycle of buying, investing, and spending by integrating mUSD with cards. The first week's growth shows that it can overcome the hurdles in the early stages of the launch. However, the dominance of existing giants shows how challenging the climb from millions to billions can be.

I don't know where this is going. MetaMask completes the financial cycle of buying, investing, and spending mUSD well by integrating mUSD with cards. The growth in the first week shows that it can overcome the hurdles in the early days of the launch. However, the dominance of existing giants shows how challenging the climb from millions to billions can be.

Between these realities, the fate of MetaMask's mUSD could be decided.